INDUSTRIAL BASE

Vital Signs 2026: Supercharging the U.S. Defense Industrial Base

NDIA graphic

Over the last three years, the National Defense Industrial Association has advocated for more focused and bipartisan attention on the interdependent link between a strong U.S. defense industrial base and effective national deterrence.

The policy dialogue started over the last three years was intentionally designed to build bipartisan support for a strong, resilient and diverse defense industry. The objective is to ensure consistent political will from policymakers in both the executive and legislative branches for the funding and changes required to modernize an archaic defense acquisition system.

This gives U.S. warfighters and civilian acquisition professionals the support they deserve and provides industry and investors with more predictability and higher confidence in making long-term investments. The work of previous administrations to advance these efforts is covered in the 2024 and 2025 “Vital Signs” reports.

This important work has expanded during the Trump administration, and there are tangible areas of bipartisan consensus — including ongoing efforts to reduce the amalgamation of acquisition laws, regulations, policies and norms, which drive a risk-averse acquisition culture.

There is also widespread agreement to build incentives for innovative and creative leadership in the Defense Department and the larger defense acquisition system, as well as an ongoing emphasis on the need to more efficiently acquire and scale commercial technology with defense applications.

Finally, there is also more focus on radically improved outcomes, with a shift away from processes rewarded for compliance and certainty — with a one-dimensional focus on cost control — to a system that evaluates a successful outcome as one in which the acquisition system expeditiously fields capabilities under operationally relevant timelines to address evolving and potentially simultaneous threats, while also being cost-effective.

These themes are prominent in the department’s Acquisition Transformation Strategy and implementation memos released in 2025 and culminate in the 2026 National Defense Strategy, which makes supercharging the industrial base its fourth line of effort.

The new strategy emphasizes the Joint Force’s “readiness, lethality, range and survivability — and ultimately, the military options [the department’s leaders] provide — are directly linked to the DIB’s ability to securely develop, field, sustain, resupply and transport the equipment and materiel that affords [the United States its] warfighting advantage.”

The end state goal is to enable the Joint Force to provide the president with “operational flexibility and agility.”

The strategy also reinforces that the department is focused on reinvesting in U.S. defense production capacity at scale, adopting disruptive technologies and removing outdated policies, regulations and practices that serve as obstacles.

For these reasons, in addition to its appreciation for the level of leadership and effort from both the executive and congressional branches in calendar year 2025, NDIA continues to emphasize the importance of reducing obstacles for companies across all sectors of the U.S. defense industrial base — regardless of the corporate model — in order for them to focus on scaled and sustained production.

The demands of this moment are obvious — the requirement is for radically different outcomes that enable stable and scalable production and prioritize speed in acquiring and employing disruptive technologies. The work association members have done over the last couple of years has culminated in a policy and political environment that is poised for the U.S. government and industry to work together to meet this moment in time.

The “Vital Signs 2026 Survey” had a record number of respondents. Private sector respondents were balanced between companies that exclusively use their own capital for research and development and those that both use their own capital and receive partial reimbursement through direct government contracts.

It is exceptionally noteworthy that corporate business models played a limited role in how private sector respondents answered questions about the pressing needs, challenges and opportunities in the survey. It is therefore important that public policy debates do not artificially set up a dichotomy that does not exist in practice.

It will take companies of all sizes and all corporate models to produce the platforms, services and technologies for the holistic suite of capabilities and capacity the Joint Force requires, particularly in an environment in which simultaneous crises and conflicts are an unfortunate but increasingly plausible scenario.

Therefore, the content and recommendations of “Vital Signs 2026” emphasize what needs to be done now to keep the momentum going.

Examples include the next steps required to unleash the innovative power of the private sector with prudent policies related to intellectual property, artificial intelligence and cybersecurity.

Concrete actions required to accelerate Foreign Military Sales, Direct Commercial Sales, co-production and licensed production to meet the goals of integrated and interoperable allied industrial bases.

The paradigm shift required to ensure stable production for critical munitions to meet operationally relevant timelines.

The additional investment and policy support to achieve the policy goals of onshoring and building more resilient supply chains.

Over the last two years, NDIA has advocated for a more synergistic partnership between the department and industry to create a shared sense of endeavor in achieving the desired end state of a strong, diverse and resilient industrial base. To fully realize a healthy, synergistic partnership, the association continues to ask government and private sector respondents a set of questions to compare where each respondent pool assesses areas of alignment and areas of misalignment.

In the 2026 survey, private sector respondents identified their most pressing issues.

They were: complex and protracted procurement processes, 66 percent; federal budget processes, 55 percent; burden and risk of compliance with government contracting requirements, 50 percent; and lack of or unclear demand signal, 48 percent.

There are two major changes from the “Vital Signs 2025” report.

First, while government respondents continue to view supply chain challenges as a pressing issue facing industry, in this year’s survey, private sector respondents listed supply chain challenges as their fifth concern, with a drop from 58 percent last year to 39 percent this year. Conversely, private sector respondents’ concerns regarding the burden and risk of compliance with government contracting requirements rose significantly from 23 percent last year to 50 percent this year.

For the government respondents, the top four most pressing issues identified were: identifying, recruiting and retaining talent or other workforce issues, 51 percent; federal budget processes, 51 percent; complex and protracted procurement processes, 48 percent; and supply chain challenges at 47 percent.

While there was a greater spread in last year’s survey responses that led to a different ordering of the concerns, this year’s government respondents identified the same top four issues as compared to last year’s survey.

In addition, while there is more alignment between the government and the private sector on the pressing challenges facing industry, it is noteworthy that the government respondents had twice as many respondents identify testing and evaluation processes, lack of education, training and/or preparation to apply acquisition processes as the private sector respondents.

As discussed extensively in the report, association members have a deep appreciation for the significant demand on the department’s acquisition community, and “Vital Signs 2026” has several recommendations on areas where industry would like this professional cadre to receive more support.

Meanwhile, as the department engages the defense industrial base on accelerating munitions capacity, it has been keenly focused on how these efforts can introduce new suppliers into the system and also what conditions are required to attract private capital.

The key challenge facing industry is how to adequately prepare for a possible future need for surge production under protracted conflict. The survey asked private sector respondents to identify the biggest barriers right now to surging capacity. The top three barriers identified were: no contract vehicle to justify expansion, 56 percent; challenges with expanding the number of technical workers, 41 percent; and access to additional capital to support expansion, 36 percent.

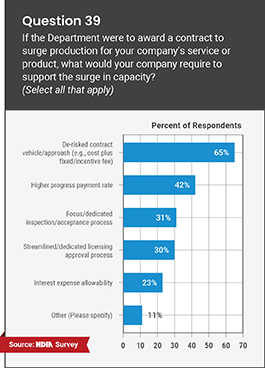

The survey also asked if the department were to award a contract to surge production, what would the company require to support a surge in capacity? Private sector respondents emphasized the importance of de-risked contract vehicles, such as cost-plus-fixed-fee/cost-plus-incentive-fee, 65 percent; higher progress payment rates, 42 percent; focused and dedicated inspection and acceptance processes, 31 percent; and a streamlined and dedicated licensing approval process, 30 percent.

NDIA met with companies representing different corporate models to elicit additional recommendations for how to immediately accelerate production. Common areas of feedback included pursuing multi-year procurements, authorizing quantity and advanced procurement funding, economic order quantities for long lead parts and yearly minimum order quantities. They also wanted award funding for long lead materials beyond current contracting and incremental testing of new suppliers and components to address government barriers around testing, qualification and acceptance.

In addition, they recommended relaxing exportability restrictions to allow for foreign production orders and qualification of allied suppliers.

The tragic conflicts around the world focusing U.S. policymakers on the current depth of U.S. munitions magazines have renewed industry’s emphasis on what is required for stable production levels. The most important method — and one the department recently announced — is the utilization of multi-year procurement authorities and the associated advanced procurement and economic order quantities funding.

These authorities are essential to help industry retain and recruit skilled workers necessary for surge production and to support their suppliers and supply chains with forecasts for long lead time items such as electronics, metal parts and steel, energetics and packing materials.

Yet, despite the challenges, the U.S. defense industrial base continues to assume risk and make capital investments. Of note, 67 percent of the survey’s private sector respondents work for companies that made significant capital expenditure investments in the last five years for either facilities and/or production lines.

Large and medium-sized industry members continue to make investments to maintain existing facilities and increase production. However, small business respondents were far less likely to report significant investments in the last five years, with only 51 percent stating that their firms had made such investments.

These small businesses may lack adequate demand signals to make these investments, and due to their smaller cash reserves, may need more concrete information to spur investment.

Additionally, further direct support may be needed so that small businesses can adequately scale up production to meet the requirements of large programs. This can be potentially ameliorated through the involvement of private equity and venture capital, which in recent years have indicated a greater desire to make investments in both defense and overall supply chains.

In addition, 51 percent of respondents indicated their companies intended to make additional significant capital expenditure investments in either facilities and/or production lines during the next five years.

Topics: Defense Contracting, Defense Department